Why are houses becoming so much more expensive to build?

Construction costs just rose at the fastest annual pace since 2005. So why is it getting so expensive to build your own home? Today we’ll look at the materials that are becoming more expensive and why all homeowners should take note – not just renovators and builders.

“Your grandpa built this place with his own two hands”, or so your dad used to boast.

So if Pop could do it with his trusty hammer, some nails, and a bit of hard yakka, why is it so expensive to build a home of your own these days? (Your own handiwork inadequacies aside…)

Well, for starters, national construction costs increased 7.3% in the 2021 calendar year alone, which was the highest annual growth rate since March 2005.

And the not-so-great news is that property market data company CoreLogic is expecting growth in residential construction costs to remain above average over the coming quarter as supply chain disruptions persist.

“There is a significant amount of residential construction work in the pipeline that has been approved but not yet completed,” explains CoreLogic research director Tim Lawless.

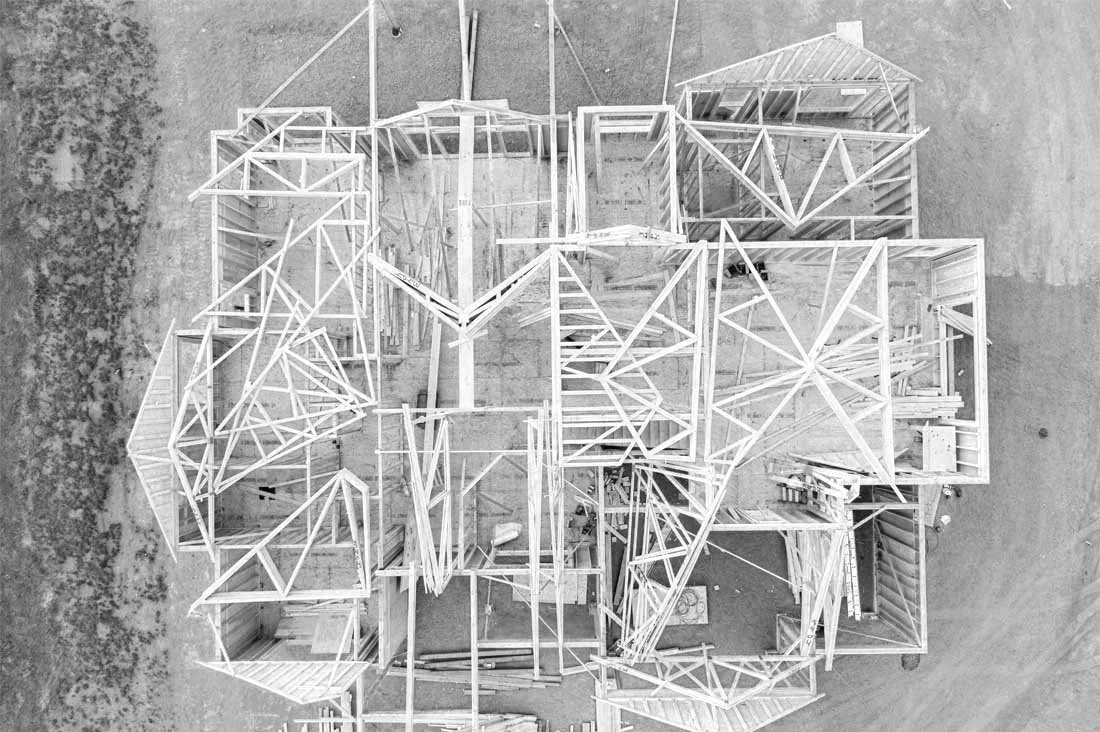

So what materials are getting more expensive and harder to source?

Data shows that cost increases are being driven primarily by timber (mostly structural timber).

In fact, in the final quarter of 2021, the value of select wood imports reached their highest level on record, says Housing Industry Association (HIA) economist Thomas Devitt.

“Timber is predominantly produced domestically but excess demand, such as in a boom year like 2022, is largely sourced from overseas markets,” says Mr Devitt.

Other segments of the market also remain volatile, with increasing pressure currently on metal costs.

“With some materials such as timber and metal products reportedly remaining in short supply, there is the possibility some residential projects will be delayed or run over budget,” adds Mr Lawless.

And with building approvals for detached housing recording their strongest year on record in 2021 (with 150,000 approvals), demand isn’t expected to slow down anytime soon.

“This boom is set to keep builders busy this year and into 2023,” adds Mr Devitt.

Mr Lawless says: “With such a large rise in construction costs over the year, we could see this translating into more expensive new homes and bigger renovation costs, ultimately placing additional upwards pressure on inflation.”

Why current homeowners should also take note

Higher construction costs are likely to add to affordability challenges in the established housing market, making it harder for homeowners to upgrade.

And CoreLogic Head of Insurance Solutions Matthew Walker warns that higher building costs mean homeowners and property investors should also review their insurance cover.

“In these times of rapidly rising home and construction costs, under insurance can quickly become a real threat to what is a most valuable asset,” says Mr Walker.

“It’s important that homeowners keep track of their sum insured and annually check that it is sufficient should the worst occur by using their insurer’s rebuild calculator or giving them a call.”

How to get the right kind of finance for a construction project

Finding the right kind of finance for a construction project can be tricky at the best of times – let alone when building supplies are becoming more expensive and wait times are blowing out due to supply constraints.

That’s why it’s important to team up with a professional like us when looking for a construction loan.

Not only can we help you secure a great rate, but we can also help you select a loan that allows flexibility for any unforeseen contingencies.

So if you’d like to explore your options for your next building or reno project, then get in touch today – we’d love to help you map out a plan for your 2022 building and property goals.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.